Yep, it’s about healthcare too:

It’s here:

|

In keeping with what has apparently become my life plan of “make comics about the fine points of healthcare policy because I can dammit,” here’s another comic about the fine points of healthcare policy. Today, our subject is the best Republican plan to replace Obamacare. There’s an article by Kurt Eichenwald in Newsweek making the rounds: “The Myths Democrats Swallowed That Cost Them The Presidential Election.” To summarize, it says:

1) The myth of the all-powerful DNC—“The idea that the DNC was some kind of monolithic organization that orchestrated the nomination ‘against the will of the people’” 2) The myth that Sanders would have won. Just to get any bias out of the way, let me say that I was a Sanders supporter—I maxed out my contributions to him—but I voted for Clinton and donated to downballot Democrats in the general. I know lots of Sanders supporters, and a few Trump supporters, but I don’t know any who didn’t vote, or who voted for Stein. (And if I did, I wouldn’t blame them for helping elect Trump unless they also live in a swing state, something that Eichenwald doesn’t mention). EDIT: Turns out I do know a couple of people who voted for Stein, but not in swing states. In any case, let’s look at those “myths.” Myth 2 is a minor point at best—Sanders could have won, as Eichenwald acknowledges, and nobody who voted for Stein cares much about a candidate’s real-world chances. It’s the first “myth”—the all-powerful DNC—that’s the meat of Eichenwald’s piece, and it’s where Eichenwald goes very, very wrong His points are: 1. The DNC itself is “an impotent organization with very little power.” This is kinda true. But it’s also missing the point. Sanders supporters’ problems were with the Democratic establishment; for most of us, “the DNC” was shorthand for that. After all, there’s a lot of overlap between the DNC and the rest of the Democratic establishment (for instance, all DNC members are superdelegates at the convention.) 2. The idea that the DNC didn’t sponsor enough debates, or that they were held at the wrong times, is ridiculous. Eichenwald is correct here. There were plenty of debates. 3. The idea that the DNC changed the rules to favor Clinton is also ridiculous. Well, except for Obama’s reform that banned donations from lobbyists and PACs to the DNC. That was changed, and people—not just Sanders supporters—were upset at the time. And it clearly benefited Clinton, who had the big-money donors locked up from the start. At the very least, this was inept—it reinforced Clinton’s “smug, corrupt, out-of-touch insider” image. And the big one: 4. The leaked DNC emails—the ones that showed the DNC collaborating with the Clinton campaign–weren’t a big deal. This is the core of Eichenwald’s argument, so let me quote him in full:

This is very very wrong. And I can prove it. Let’s start with this:

Certainly, Sanders had an uphill battle from the beginning. But he “could not possibly have won the nomination after May 3”? That didn’t square with my recollection. So I went and checked. After his victory in the May 3 primary, Sanders had 1400 delegates or so (sources conflict); he needed 2,383 to get the nomination, which meant he needed more than were still available in the remaining primaries. So Eichenwald sounds correct. But here’s the problem: Eichenwald’s math assumes that Sanders wasn’t going to get a single additional superdelegate—that all of Clinton’s superdelegates would stay with her no matter what. And remember, in the very next paragraph, Eichenwald says this:

But only one of the following can be true: Either Sanders only needed to win the most pledged delegates, and then the superdelegates would have rubber-stamped the decision of the people, Or Sanders needed to also win a whole lot more pledged delegates in order to overcome a bloc of superdelegates who were going to vote for Clinton no matter what. If the first is true, Sanders’s path to victory after May 3, while very difficult, was not impossible; it didn’t become truly impossible until June. In that case, the DNC had no business jumping into bed with the Clinton campaign in May. If the second is true, then Eichenwald is right that the emails are innocent, but the Democratic establishment was ready and waiting to enact a scenario that Eichenwald calls, in the very next paragraph, “an establishment overthrow of the electorate more common in banana republics or dictatorships.” Either way, Sanders supporters have a legit grievance here. And somehow Eichenwald forgets that it wasn’t just Sanders supporters who were upset at the DNC’s conduct. Here’s Ed Rendell on the subject of those emails: “Myself and other Democrats who were Clinton supporters, we have been saying this was serious. It truly violates what the DNC’s proper role should be. . . . The DNC did something incredibly inappropriate here.” “Serious.” “Incredibly inappropriate.” Rendell is former Governor of Pennsylvania and former chair of the DNC. He’s not some dreamy hippie—he’s as much of a party insider as one can be. There was a reason Debbie Wasserman Schultz resigned, after all. And remember: Clinton immediately welcomed her onto her campaign, in a smug, inept fuck-you to everyone except the Democratic elite. Eichenwald chooses not to mention this colossal own goal. Point being, if liberals had a problem with Clinton and the Democratic establishment, there’s no reason to look for “provably false conspiracy theories.” There were plenty of legitimate reasons. Like the fact that Clinton was clearly a dangerously flawed candidate, and it wasn’t just us who thought so. Here’s a thoroughly mainstream reporter:

That reporter? Eichenwald himself, after the primary was over. And let’s not forget the behavior of the Democratic establishment. Sanders supporters didn’t have legitimate worries about running a candidate who already had a 20-year-old industry devoted to hating her, who was such a bad campaigner that she nearly flubbed a locked-up primary against a goofy socialist, who was one of the most unpopular presidential candidates in history. Rather, we were being childish, refusing to be grow up and go with the “electable” candidate. We were sexists (never mind that almost all of us would have switched to Elizabeth Warren if she’d run). We weren’t worried that Clinton could very possibly lose in the general, we were just whining because our needs weren’t being catered to. We didn’t have legitimate reason to believe that our political insiders were not offering real solutions to urgent problems (as I write this, the arctic is 36 freaking degrees warmer than normal), we were trying to impose our own left-wing dictatorship. I’m not exaggerating. Here’s a pro-Clinton journalist during the primary:

“The type of movement through which tyrants are born.” That’s, um, a tad hyperbolic. Is it strange if Sanders supporters (sorry, “Berniebros”) were turned off? And that reporter? Yup, Eichenwald himself, in a piece telling Sanders to get out of the race. (Never mind that Clinton stayed in the 2008 race long after she had no path to victory, and when asked why, came up with this gem: “We all remember Bobby Kennedy was assassinated in June in California.” So she was sticking around in case someone shot Obama. Imagine Eichenwald’s outrage if Sanders had said anything so divisive.) Oh, and the end of that piece (which, remember, was written during the primary) is instructive:

That reads as a not-very-veiled threat—run Sanders and many Democrats won’t vote for him and it’ll be Sanders’s fault, not theirs. Even if it wasn’t intended as a threat, the message is clear: When the democrats ran a liberal and “a large segment of the usual party supporters” stayed home or voted for the opponent, the candidate was to blame. But when a (much smaller) segment of the usual party supporters stayed home for Clinton, they’re to blame. Because she was the serious, grown-up choice, you see. Bullshit. We are facing the horror of President Trump—which really could lead to a tyranny—for many reasons, but a big one is that the Democratic elite shat the bed. They lined up behind a flawed, uninspiring, insider candidate in a year when the voters—not just some precious lefties, but everyone—clearly demanded something else. And now Kurt Eichenwald is telling us that we should go home, stay out of the way, and vote for whatever “electable” candidate (which means, as far as I can tell, “electable except for all the assholes who won’t vote for him or her”) the elite wants to lose with next time. He can go have sex with himself, and I mean that in much cruder terms. Feeling a bit stabby today? Here’s something to do: If you still have a Democratic representative or Senator, write them a letter. An honest-to-God, peel-the-stamp-and-stick-it letter. Tell them that you expect them to fight Trump’s disastrous agenda. And that if they roll over for Trump, you will support—with your vote, with your donations, and with your time—any primary challenger who willfight Trump’s agenda. Follow through on that. If they stand up to Trump, support them in all those ways. If they don’t, support a challenger. Actual letters do more than emails or internet petitions. Get the addresses here: https://www.usa.gov/elected-officials. So, back in early 2016 Dan and I did a timeline of economists and economic thought for Les Arènes, the publisher of the French translation of Economix. For you French folks, it is (or was?) available in hard copy with a purchase of the book. For the rest of y’all, here it is: https://economixcomix.com/timeline-of-economists/. French fans: I’ll be in and around Paris starting the end of this week: April 30: A book signing at BDNET Bastille, 26 rue de Charonne, at 16h00 May 1: A talk with Laurent Cordonnier at Salon du Livre in Arras at 16h15 (Information here) May 4: Interview and Q&A at La Maison de Université in Rouen Come and soak up the geekiness! (The autocorrect kept trying to make that last word “meekness” . . .)

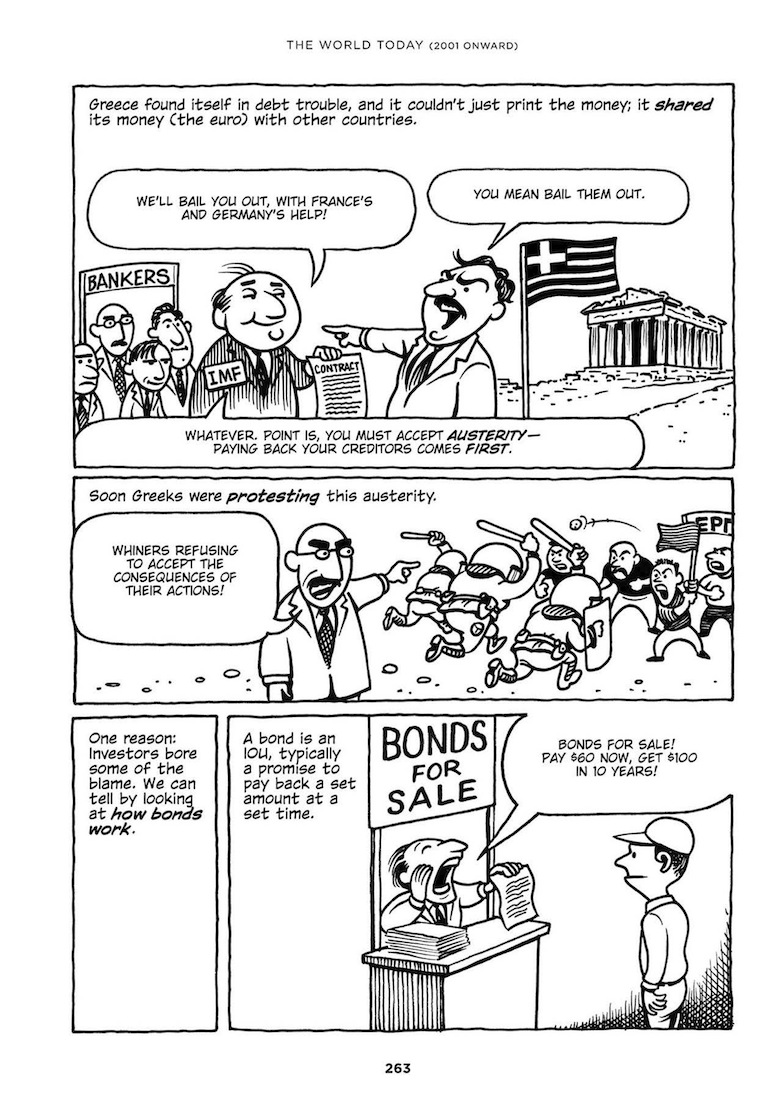

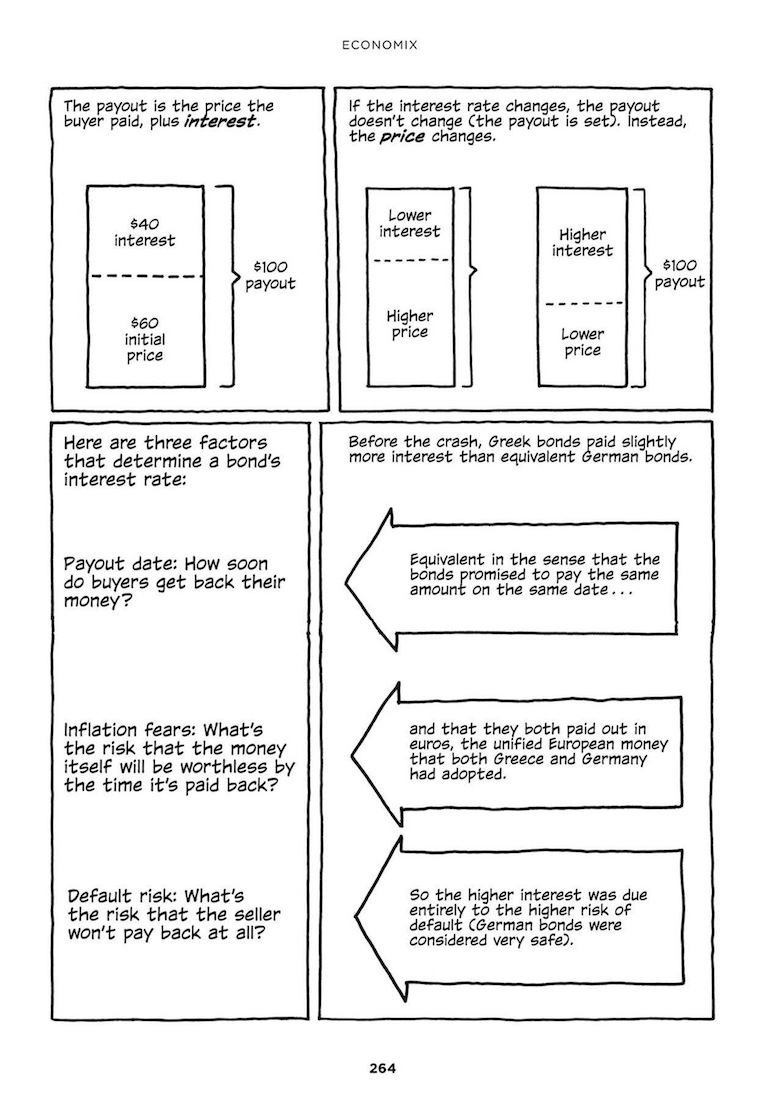

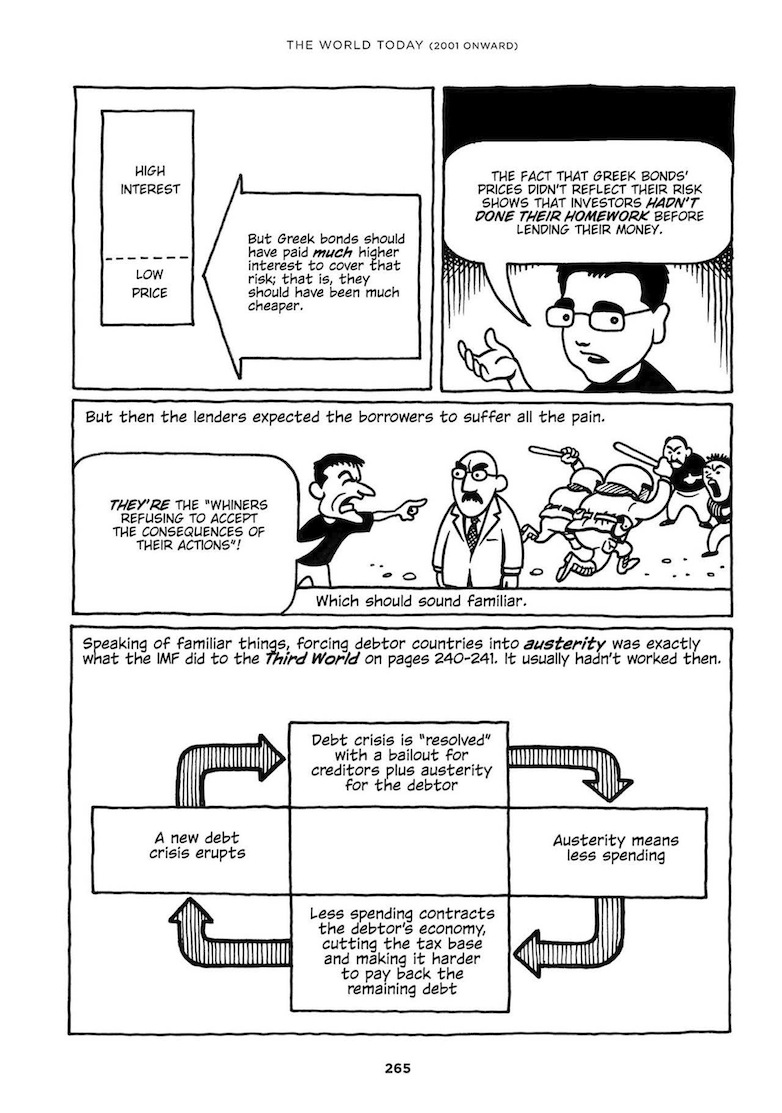

So, the Greek referendum is today. Here’s hoping that it forces some progress in the endless madness that is the Greek crisis. Because so far the Troika has simply been demanding the same things, in the same terms, for years. Is it even a “crisis” when nothing changes for that long? Seriously, check out what I wrote about Greece in Economix, keeping in mind that the text was finished in mid-2011. I would write the same thing word for word today.

That’s been the situation for the last four years and more. But maybe not tomorrow.

EDIT, 7/5/2015: When I wrote this I was confused by the holiday and thought it was already Sunday. Derp.

WARNING: See edit below. So, NASA is now predicting that the remnants of the Larsen B ice shelf will be gone by the end of the decade. I’m going to make my own prediction, just so I’m on the record: It’ll happen faster than that. This coming summer (the Antarctic summer, so Winter 2015-2016 here) or the summer after. No, I have no access to climate data that NASA doesn’t have. And I don’t read the data better than climate scientists do, or at all. But I’m still pretty confident. That’s because, in a weird way, the right wing is correct: Climate scientists are always wrong. They’re wrong because they start from the assumption that nothing will change. Then they look at the data and report upcoming changes that they can prove. The researchers have no real choice in this; anything less rigorous would leave them open to a slew of well-funded attacks from deniers. So, for instance, nobody knows what the impact of methane release from melting permafrost will be. Climate models therefore don’t take it into account, because any value they gave it would be a guess. But giving it a value of zero is also a guess, and almost certainly a worse guess than any positive value they would have given it. And so again and again, what scientists can prove at any given time is overtaken by events soon after. So if climate scientists say the Larsen B shelf will be gone in five years, I’m pretty sure it’ll be quicker than that. Let’s hope I’m wrong. EDIT: Reader Fabius Maximus has pointed me to several cases in which reality has not been as bad as climate scientists have predicted. I’m not sure why I hadn’t come across these–it may have been my personal bad-news bias, or the fact that “problems worse than scientists predicted” makes a better headline than “problems in the low end of the predicted range.” So, my bad. The lesson here, kids, is don’t listen to nonscientists about the freaking climate. So anyone who read my rant about N. Gregory Mankiw’s atrocious textbook knows I’m not a big fan. Now comes Mankiw’s recent op-ed in the Times supporting the Trans-Pacific Partnership and the Transatlantic Trade and Investment Partnership: “Economists Actually Agree on This: The Wisdom of Free Trade.” It reminded me of another piece: Sylvia Nasar’s column supporting NAFTA in the very same paper, 23 years ago: “A Primer: Why Economists Favor Free-Trade Agreements.” Here’s the first line of Nasar’s article:

So economists were unanimously for free trade 23 years ago, and they’re unanimously for it now. Free trade is therefore good. Q.E.D., right? Well, it’s worth reminding ourselves why economists were for NAFTA back than. Nasar wasn’t arguing that NAFTA would be great for the US; rather, she was saying that the effect on the US would be minor, while it would be great for Mexico (and that a prosperous Mexico was in the US’s interest). So what happened? Mexico’s wages have stagnated to the point that Mexican wages are now lower than Chinese ones. And politically, rather than a prosperous neighbor, we have a country that has teetered on the edge of becoming a failed state. And while one could argue that it’s not NAFTA’s fault, one would be wrong. NAFTA actually does deserve a lot of the blame here. So how can economists, after 23 years’ worth of evidence that they were wrong, have learned nothing? How can they still agree that NAFTA-style “free trade” agreements (which is what the TPP and TTIP are) are simply good? Well, part of the answer is that Mankiw is lying. Some economists have learned from their mistakes. The consensus is not nearly as strong as it was in the 1990s, when the only debate was between economists who thought that trade agreements were flat-out good and those who acknowledged that they might not be good for every person unless the winners compensated the losers out of their winnings. But the rest of the answer is that Mankiw is a poster boy of what’s wrong with too many economists (perhaps in part because so many economists start with his atrocious textbook): he sees the world as a set of postulates and theorems, and he sees no reason to abandon that approach just because facts don’t agree. So when he says

That’s because to him, it’s just axiomatic that our policies can’t affect the number of jobs (scroll down to “The Broken Window Fallacy Fallacy” here if you want to see why I disagree). Then it gets worse. Far, far worse. The second part of Mankiw’s article, and seemingly the real point, speculates on why we, the voters, just won’t listen to economists on trade. Here’s Mankiw:

Is his answer: “Because economists have been sure and wrong before, and a rational person can doubt whether the same justifications that have proven wrong in the past are correct today?” No! Check this out:

If you’ve finished laughing about “fully rational politicians” let’s — you haven’t? I’ll wait. . . . Okay, take a minute to read it again. Read Mankiw’s smug condescension: you stupid voters just don’t understand. Only he understands. Mankiw is giving what are basically the core beliefs of the econ profession:

Thing is, only the first point is true. Economists’ models are certainly opaque to the rest of us, but they have a truly atrocious track record, and most economists simply don’t care. No other field, except perhaps astrology, fetishizes its methods to the exclusion of its results; no other field looks down on people who check to see what happens in the real world. So when Mankiw says this:

He’s describing himself, not voters. Mankiw, not voters, is “worse than ignorant about the principles of good policy.” And yet he thinks we should have *less* of a voice in our own government. How the fuck does this guy get to keep his chair at Harvard? “I observe that, although the speeches on our side are always manifestly just and sympathetic, and . . . are always regarded as saying what ought to be said, yet practically nothing is done which ought to be done, or which would make it worth while to listen to such speeches.” —Demosthenes, Second Philippic, ~344 BC Apropos of nothing, of course. |

Buy the book:

| |